Financial Red Flags to Avoid in Your 20s and 30s

Your 20s and 30s are the most critical financial decades of your life. During this window, you possess a mathematical superpower that you will never have again: a massive, decades-long runway for compounding interest to work its magic. Yet, these years are also a minefield of societal pressures, lifestyle adjustments, and seemingly minor financial habits that can quietly sabotage your economic independence before it ever gets off the ground.

Welcome to The Financial Red Flags Survival Blueprint. In your early career, it is incredibly easy to mistake a rising cash flow for genuine wealth accumulation. Without an analytical defense system, you can easily fall prey to systemic consumer traps that lock you into a cycle of permanent financial anxiety. Today, we will break down the absolute most dangerous financial red flags to avoid in your 20s and 30s, and show you exactly how to pivot toward absolute autonomy.

The Predator Red Flags: Destructive Financial Habits Deconstructed

Many of the worst financial traps don't look like emergencies when they first appear. They look like completely normal, everyday lifestyle choices, hiding their long-term destructive power under the guise of convenience, status, or standard adult progression.

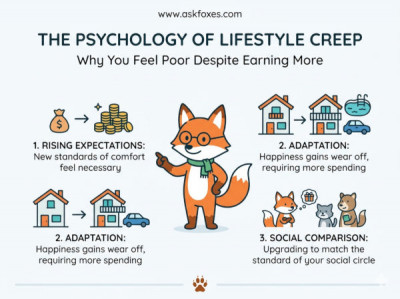

1. Running on the Endless Hedonic Treadmill

As you secure promotions and scale your income streams, letting your discretionary spending rise in exact lockstep is a massive behavioral red flag known as lifestyle creep. Your brain quickly reclassifies past luxuries into baseline necessities, leaving your savings rate completely stagnant despite a higher tax bracket. When your spending curve mimics your earning curve step-for-step, you trap yourself in a state of perpetual golden handcuffs.

2. The Minimum Payment Loophole

Carrying credit card balances or relying heavily on "Buy Now, Pay Later" frameworks is a critical warning sign that your lifestyle has outpaced your actual liquid means. Lenders purposely structure minimum payments to maximize their corporate interest revenue while keeping your principal balance intact for decades. If you are paying high double-digit APR percentages to fund past consumer choices, your cash flow is actively being drained by corporate profit centers.

3. Leaving Cash to Melt Under Inflation

While establishing an emergency fund containing three to six months of living expenses is a vital personal finance rule, leaving those total cash reserves sitting in a traditional, big-box bank account paying a dismal 0.01% interest rate is a quiet wealth-killer. When consumer price indexes outpace your banking yields, your idle capital is actively losing real purchasing power every single day. Cash safety is essential, but leaving it unprotected from currency devaluation is financial madness.

The Behavioral Divergence Matrix

Recognizing the difference between a high-risk lifestyle profile and an optimized financial trajectory requires looking at the subtle choices that compound over a twenty-year career window.

| Financial Category | The High-Risk Red Flag Scenario | The Strategic Sovereign Shift |

|---|---|---|

| Income Influx Shifts | Discretionary spending inflates immediately to match higher net intake. | Utilizing reverse budgeting to automate 50% of any raise straight into investments. |

| Emergency Capital Storage | Leaving defensive cash in a traditional checking or low-yield savings tier. | Moving liquid reserves to an online, Member-FDIC High-Yield Savings Account (HYSA). |

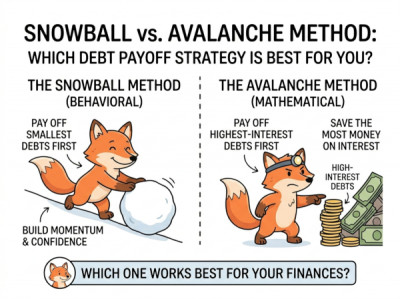

| Debt Optimization | Paying only mandatory minimums while continuing to swipe revolving cards. | Deploying the psychological Debt Snowball or mathematical Debt Avalanche framework. |

| Wealth Perspective | Defining success via loud, visible status symbols and material acquisition. | Deriving status from invisible balance sheet strength and absolute time freedom. |

The 4-Step Blueprint to Purge Red Flags and Lock in Autonomy

To successfully purge these critical wealth-leaks from your financial layout and protect your peak compounding decades, execute this uncompromising operational framework:

- Step 1: Execute a Complete Statement Audit. Log into your portals, bypass the simplified mobile app dashboard summaries, and download the comprehensive, itemized statement PDFs for the last 60 days. Look closely for hidden convenience leaks, unutilized app subscriptions, and crammed fee structures.

- Step 2: Enforce a Psychological Spending Cooldown. Combat impulsive consumption and social mimicry by introducing a mandatory 72-hour delay on any discretionary purchase that exceeds $100. Forcing an intentional cooling window allows your logical mind to clear out the initial dopamine spike and evaluate the item's true utility.

- Step 3: Capture Fractional Ownership Early. Stop waiting for a massive lump sum of cash to begin building your market safety net. Democratize wealth creation by utilizing modern micro-investing apps to consistently route automated spare-change round-ups or tiny $5 weekly recurring deposits into diversified broad-market ETFs.

- Step 4: Establish an Independent Banking Buffer. Separate your daily transactional spending environment from your defensive accumulation pools. Move your core emergency reserves to a dedicated high-yield digital tier that is completely unlinked from your daily debit card, rendering your safety net out of sight, out of mind, and safe from emotional dipping.

"The ultimate luxury in your 20s and 30s isn't projecting wealth to a world of strangers; it is possessing the absolute, quiet sovereign freedom to control your own time." — The Autonomy Imperative

The Financial Reset Execution Script

When restructuring your banking configuration to systematically eliminate behavioral risks, do not rely on your daily human willpower. Program your banking layout to run like a strict, automated machine that filters out wealth degradation before it can manifest. Configure your digital rules using this precise system logic:

By identifying these early financial landmines and taking deliberate, proactive control of your wealth trajectory, you shift from a passive participant in consumer culture to an active capital allocator. Avoid the traps that keep the crowd financially trapped, lock in your compounding engine, and secure the clean financial path required to claim your lifelong personal and economic sovereignty.